China leading manufacturers and suppliers of Meat Grinder,Meat Grinder Parts, and we are specialize in Meat Grinder Spare Parts,Stainless Steel Meat Grinder, etc.

Jiangmen Hongyi Electrical Appliance Manufacturing Co., Ltd. is a professional enterprise which aims at producing household electrical appliances. Our company is located in Jiangmen City, Guangdong Province. We are adjacent to Guangzhou, Shenzhen, Macao and Hong Kong. The transportation is very convenient.

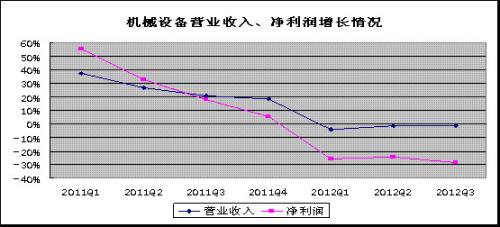

Meat Grinder,Meat Grinder Parts,Meat Grinder Spare Parts,Stainless Steel Meat Grinder Jiangmen HongYi Electrical Appliance Manufacturing CO.LTD , https://www.hyappliances.com The performance of listed companies in the machinery industry has been relatively sluggish this year. According to wind data, the 282 listed companies of Shenwan Machinery and Equipment achieved operating income of 632.088 billion yuan and net profit of 37.416 billion yuan for the first three quarters of 2012, a year-on-year decrease of 1.38% and 28.27% respectively. . The data also shows that since the first quarter of this year, the growth rate of listed company's revenue growth has slowed down. However, due to the continued decline in gross profit margin, the growth rate of net profit continued to fall in the first three quarters.

The performance of listed companies in the machinery industry has been relatively sluggish this year. According to wind data, the 282 listed companies of Shenwan Machinery and Equipment achieved operating income of 632.088 billion yuan and net profit of 37.416 billion yuan for the first three quarters of 2012, a year-on-year decrease of 1.38% and 28.27% respectively. . The data also shows that since the first quarter of this year, the growth rate of listed company's revenue growth has slowed down. However, due to the continued decline in gross profit margin, the growth rate of net profit continued to fall in the first three quarters.

From the perspective of the sub-sectors, construction machinery benefited from the traditional construction season in the second half of the year and the country's investment in railway infrastructure has rebounded, and the industry’s economy has been slowly picking up. However, at present, the recovery of downstream demand is weak, and it is difficult to provide substantial support for the growth of the industry. In general, the construction machinery industry is still in the down cycle. Despite the abundant reserve of downstream engineering projects, the sources of funds for project construction are tense. It is still to be seen whether the construction equipment can be significantly improved in the last two months. According to the data from the Construction Machinery Network, China’s cumulative sales of bulldozers, loaders, cranes, and rollers from January to September were 7,579, 138, 341, 17,957, and 10,862, respectively, representing a year-on-year growth rate of -31.60%, -27.99%, and -38.84 respectively. %, -40.66%, a sharp decline from the same period last year.

In terms of machine tools, due to the unclear trend of the manufacturing industry in China, and the decline in the profit rate of manufacturing companies, the willingness of companies to upgrade their processing equipment and expand investment is low. In the next two to three quarters, the possibility of improvement in the market demand for machine tools and the profitability of machine tool manufacturers in China will remain relatively small.

In the shipbuilding industry, the economy in the fourth quarter may continue to deteriorate, and 2013 may face even greater difficulties. On the one hand, the demand for downstream shipping is still sluggish. On the other hand, from the perspective of current orders, the value of the delivery of civilian vessels in the future of China Heavy Industry, China Shipbuilding, Guangzhou Shipyard International and other industries is still declining.

The military industry has benefited from the favorable influence of territorial disputes and policies, and the business climate is expected to continue to rise. The situation in the fourth quarter of the Diaoyu Islands is expected to continue to be tense, after the 18th National Aeronautical Aeroengine major special plan will speed up the approval process, before the end of the low-altitude airspace top management methods and navigation subsidies policy is expected to be introduced. In addition, large-scale military transport aircraft developed by China at the end of the year are expected to enter the test flight stage and begin small-scale production next year.

In terms of railway infrastructure, although the national railway fixed asset investment of 630 billion yuan is still under pressure during the year, from the aspect of stable economic construction, the possibility of completion is relatively large. In the fourth quarter, the average monthly investment in railway fixed assets is expected to reach 95.3 billion yuan. Yuan, a 50% increase from the fourth quarter of last year, so the railway machinery sector will continue to enjoy the policy dividend. In addition, from the perspective of demand, the steady advancement of EMUs, locomotives, and trucks in the second half of the year is a high probability event.

Finally, from the perspective of the prices of major raw materials in the upstream market, the spot prices of major steel products representing infrastructure and machinery demand have continued to decline in the near future, and the overcapacity of steel production will continue. Since October, steel prices have stabilized and recovered, but they are still at a low level.

In terms of coal, due to the sharp drop in natural gas prices in the United States, the share of coal in primary energy in the United States has decreased, resulting in the continued decline in domestic coal prices since the beginning of the year. Recently, domestic coal prices have shown some signs of stabilizing, but the recent decline in foreign coal prices is likely to curb the rebound in domestic coal prices.

In terms of crude oil, international crude oil prices have been falling rapidly since March 2012 due to factors such as weak US economic data and uncertain outlook for the euro zone. After Saudi Arabia, the world's largest oil producer, considered rumors of increased oil output and the Fed announced the launch of the third round of quantitative easing measures (QE3), investors opted to sell at high levels, leading to a sharp correction in oil prices.

In summary, the prices of major raw materials in the machinery industry are generally at a low level, which is beneficial to enterprises in reducing production costs, but it also reflects that the machinery industry is still in a weak state.

Overall, the current domestic economy has shown a trend of stabilizing and recovering, and the steady growth policy has been continuously strengthened recently, providing certain support and structural opportunities for the development of the machinery industry. However, due to the fact that the market inventory remains high and there are many uncertainties in the economic recovery, the overall recovery of the machinery industry will take time.

Judging from the trend of the industry index, the mechanical index recently re-formed the trend of sideways bottoming after falling below the bottom of the box, and set a new low in the past three years in the previous week, as the previous sideways accumulated more traps, the market rebounded The resistance encountered will be very obvious.

Our company has product development, mould manufacturing, testing, product manufacturing and other departments. We have a professional team to ensure product quality. We provide quality and high performance products for clients. Our company aims to establish good and stable trade relationships with clients. Our products are exported to Southeast Asia, the Middle East and other countries and regions. We have deeply won consumer's trust.

Our main products are food mixers, blenders, electric fans, electric irons, plastic accessories and hardware.

Our company has consistently adhered to the concept of "outstanding quality, affordable price, excellent service". We hope to strengthen economic cooperation with friends from all over the world and create a bright future together.